Introduction

Oregon was the second state in the U.S. to adopt a Low Carbon Fuel Standard (LCFS) similar to California’s. In 2009, the state authorized a 10% reduction in transportation fuel carbon intensity over 10 years. By 2015, the Clean Fuels Program (CFP) was fully implemented, aiming for a 10% reduction by 2025. The state later expanded the goal, targeting a 20% reduction by 2030 and 25% by 2035. The CFP sets annual carbon intensity (CI) standards for gasoline, diesel, and alternative fuels, requiring fuel providers to meet targets or buy credits. It mirrors California’s LCFS, allowing approved fuel pathways from California to be used in Oregon.

In this piece, we will delve into the details of Oregon Clean Fuel Program, examining the major credit and deficit generating fuel, change in share of carbon generated credit by low-carbon fuel type over time, outlook of the program, and the trend in carbon intensity for renewable diesel by 2030.

Renewable Diesel – Major credit and deficit generator

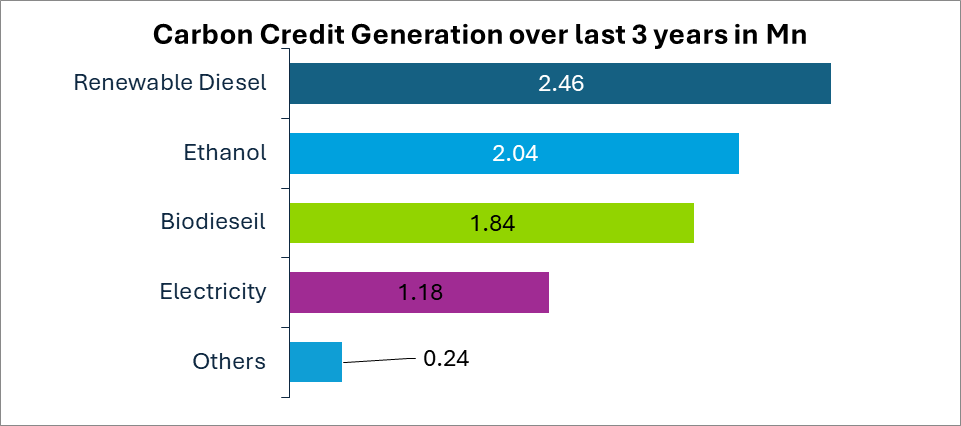

As shown in Figure 1 below, renewable diesel has been the leading generator of carbon credits in Oregon over the past three years, producing 2.4 million credits. It is followed by ethanol and biodiesel, which generated 2 million and 1.8 million credits, respectively

Figure 1:

Carbon Credit Generation over last 3 years in MT

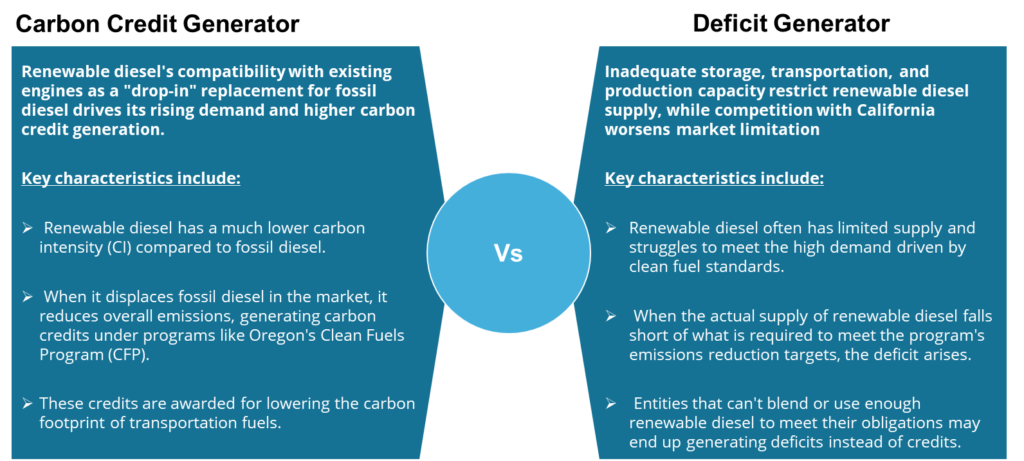

A fuel like renewable diesel can act as both a carbon credit generator and a deficit generator due to its unique role in clean fuel programs:

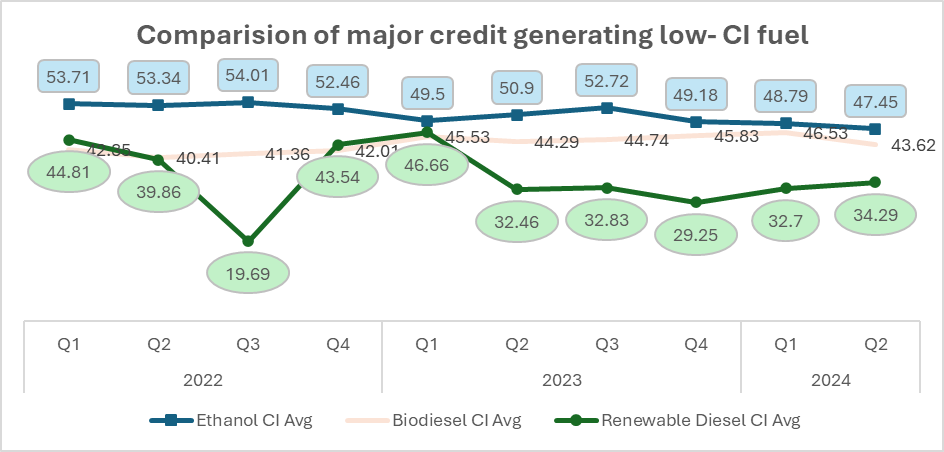

As illustrated in Figure below, the average carbon intensity (CI) of renewable diesel is lower than that of other major credit-generating clean fuels, such as ethanol and biodiesel. This is largely due to its use of waste-based feedstocks, efficient production methods, and compatibility with existing diesel infrastructure, making it a cleaner and more sustainable option.

Reasons Behind Renewable Diesel being a major Carbon credit generator in Oregon

High Demand for Low-CI Fuels

Renewable Diesel as a Low-CI Fuel: Renewable diesel has a significantly lower CI compared to fossil diesel, often approaching net-zero emissions when produced from waste feedstocks like used cooking oil or animal fats. Producers and suppliers of renewable diesel generate credits because they help the state achieve its CI reduction targets.

Fossil Diesel Substitution

Oregon relies heavily on diesel fuel for freight and transportation, which typically has a higher CI than the program’s targets. Renewable diesel is one of the few “drop-in” substitutes for fossil diesel, meaning it can be used in existing engines without modifications. When renewable diesel is available, it offsets fossil diesel usage, generating credits.

The low CI of renewable diesel

Renewable diesel, made from waste-based feedstocks like used cooking oil and animal fats, has a lower carbon intensity due to repurposing waste and efficient hydrotreating processes. In contrast, ethanol and biodiesel rely on agricultural feedstocks, involving emissions from land-use changes and energy-intensive production, making them less efficient and higher in CI.

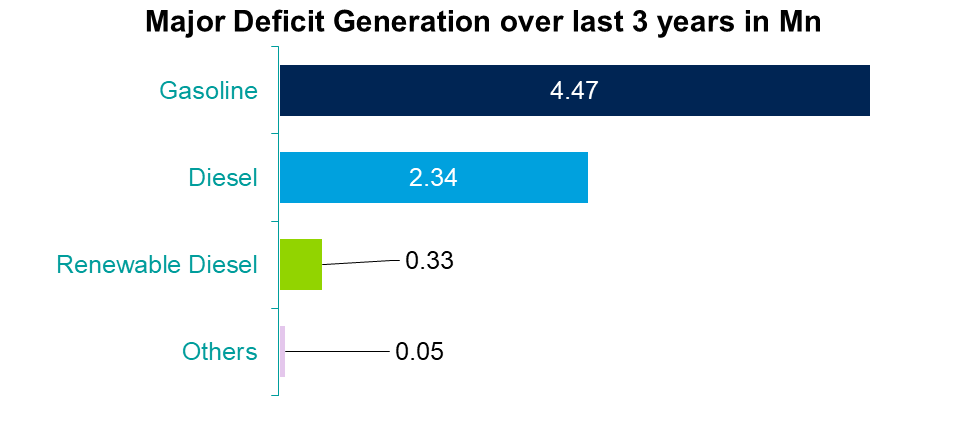

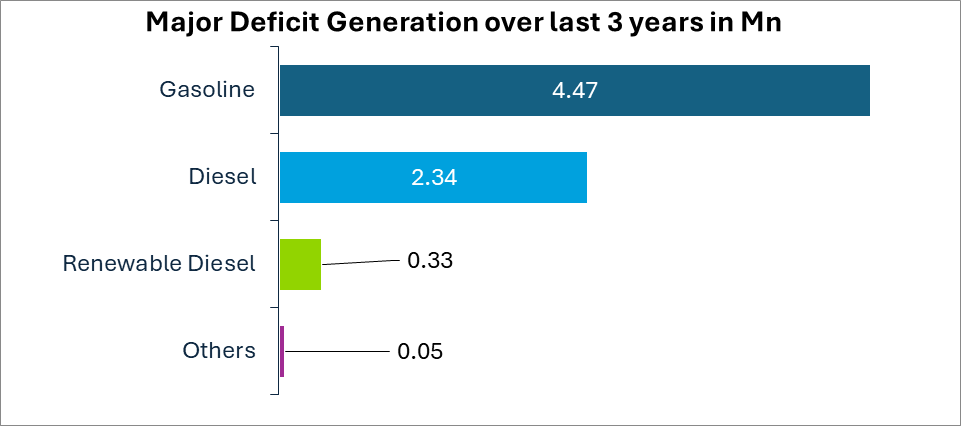

As depicted in Figure 3, renewable diesel has been a significant contributor to deficits among low-CI fuels, ranking behind gasoline and diesel, which are high-CI fossil fuels. Over the past three years, renewable diesel has generated a deficit of 0.3 million credits in Oregon.

Factors Contributing to Renewable Diesel’s Deficit Generation in Oregon

Limited Storage and Transportation Capacity

Renewable diesel deficits in Oregon are partly due to inadequate storage and transportation infrastructure. Federal and state labeling regulations require renewable and petroleum diesel to be stored separately, necessitating the construction of dedicated storage tanks or the conversion of existing infrastructure. This limits the quantity of renewable diesel that can be imported. In contrast, California, with its well-developed storage infrastructure, can accommodate larger imports, supporting its clean fuel program effectively.

Oregon’s demand for low-CI fuels like renewable diesel often exceds the available supply, creating deficits for entities that cannot access or supply enough renewable diesel

Limited Production Capacity

Oregon lacks renewable diesel production facilities and depends entirely on imports. In comparison, California has a production capacity of approximately 184 million gallons per year (7% of the U.S. total) from refineries such as the Marathon Martinez refinery (23,000 bpd) and Phillips 66 refinery (12,000 bpd). Several refineries in California are also planning expansions, further increasing their output in the coming years.

When renewable diesel is unavailable or insufficient due to limited production capacity, deficits occur due to the continued reliance on high-CI fossil diesel

Smaller Market Size

Oregon’s diesel consumption is about one-fourth of California’s, making it a comparatively smaller market. As a result, more renewable diesel is directed to California, where the larger market size and infrastructure support higher demand.

Oregon’s smaller market size and competition with California for renewable diesel result in limited supply, forcing reliance on high-CI fuels and generating credit deficits under the state’s Clean Fuels Program.

Renewable Diesel – generated the highest fraction of credits in the last 3 year

Since the launch of the Clean Fuels Program (CFP), the proportion of renewable fuels in Oregon’s total generated credits has increased, with renewable Diesel emerging as the leading renewable fuel in credit generation, as illustrated in the figure below.

Fig 4: Change in share of carbon generated credit over time

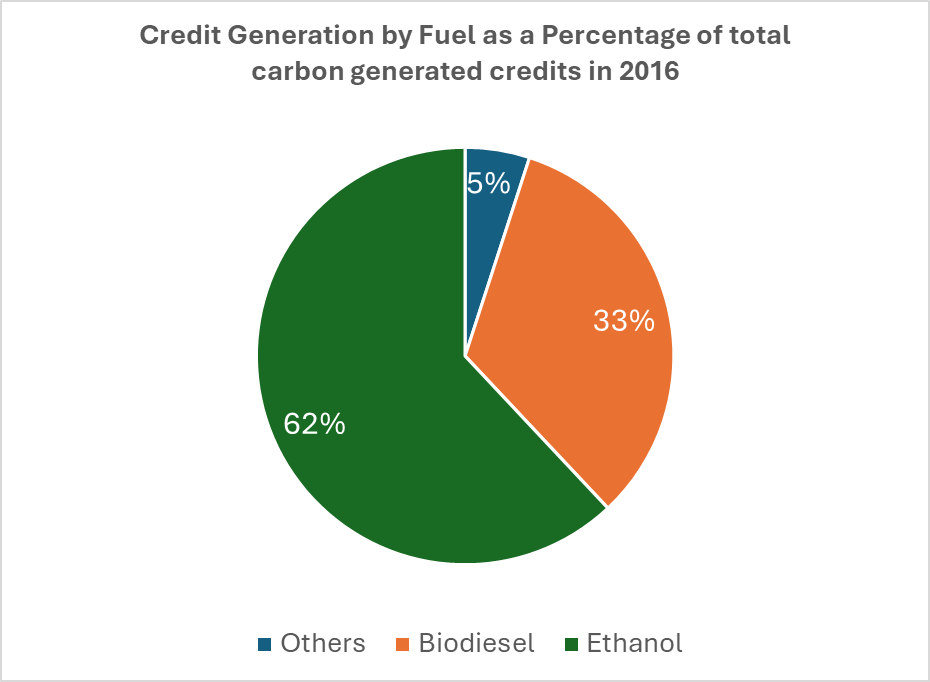

From 2021-2024, credit-generating fuels consisted of renewable diesel (31%), ethanol (26%), biodiesel (23%) and electricity (15%)This contrasts with 2016, the first year of Oregon CFP reporting, when nearly 95% of credits came from just two fuels: ethanol (62%) and biodiesel (33%).

Outlook for Oregon clean fuel program by 2030

The state department asserts that achieving a 20% carbon intensity (CI) reduction target will encourage a diverse range of low-carbon fuels to compete as replacements for gasoline and diesel. These fuels include ethanol, biodiesel, renewable diesel, renewable natural gas, renewable propane, electricity, hydrogen, and others.

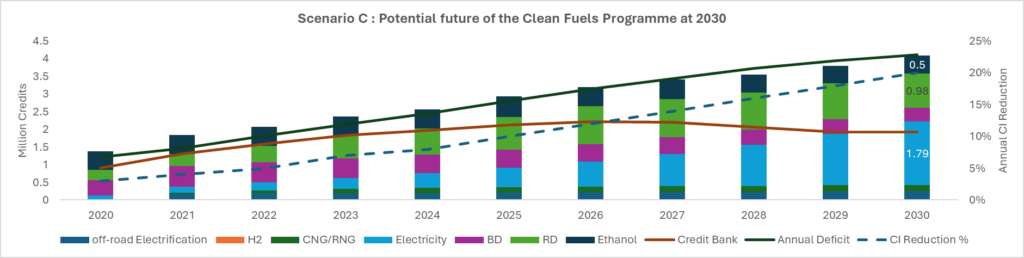

To evaluate compliance, ICF developed two scenarios: Scenario A, which focuses on a single compliance pathway, and Scenario C, which integrates multiple fuels for a more comprehensive approach.

Scenario C, considered more holistic, includes liquid and gaseous fuels alongside electricity, resulting in a projected 20% CI reduction by 2030. This reduction aligns with blend rates and CI values reported through the Clean Fuels Program (CFP) and corroborated by other jurisdictions.

The modelling indicates that achieving a CI reduction target above 20% by 2030 is crucial to leveraging contributions from all fuel types. While future regulations aim to transition most vehicles to zero-emission models, the continued demand for low-carbon liquid fuels will persist for decades. A higher target will sustain incentives for investments in low-carbon fuel alternatives like ethanol, biodiesel, and renewable diesel, ensuring these fuels maintain a significant market presence.

Trend in carbon intensity for renewable diesel by 2030

The carbon intensity (CI) of renewable diesel is expected to decline by 2030, driven by advanced technologies, better feedstocks, and regulatory incentives promoting low-carbon alternatives.

Cleaner Feedstocks and Process improvements

Technological advancements are enhancing efficiency, reducing energy consumption, and lowering emissions. Adopting alternative feedstocks and innovative technologies like Gasification Fischer-Tropsch (GFT)), Power-to-Liquid (PtL), and hydrothermal liquefaction offers promising low-carbon solutions. Usage of these newer technologies use feedstocks that cost less and have lower carbon intensity.

Policy Incentives

Programs like the Oregon Clean Fuels Program (CFP) and California Low Carbon Fuel Standard (LCFS) set annual CI reduction targets. These policies incentivize renewable diesel producers to continuously innovate and achieve lower CI scores. Oregon aims to reduce the average carbon intensity of transportation fuels by at least 20% compared to 2015 levels by 2030 and 25% by 2035, setting one of the most ambitious targets in the United States.

Shift in Transportation Sector

Electric vehicle will dominate the dominate Oregon CFP by 2030. Increased demand for renewable diesel in sectors where electrification is challenging will encourage production of ultra-low-CI fuels to meet stricter compliance requirements.

Conclusion

Oregon’s Clean Fuels Program takes a significant step toward reducing greenhouse gas (GHG) emissions, driving innovation in clean energy, and tackling climate change through market-driven solutions. An analysis of the past three years of data shows that renewable diesel has played a dual role as both the largest credit and deficit generator in the state’s carbon credit system. Renewable diesel generates credits by reducing emissions due to its low carbon intensity, achieved through waste-based feedstocks and efficient production methods. However, limited supply and high demand can lead to deficits when clean fuel targets are unmet, underscoring its unique position in the program.

The analysis also reveals that renewable diesel has a lower average carbon intensity (CI) compared to other major credit-generating fuels like ethanol and biodiesel. Its reliance on waste-based feedstocks, advanced production methods, and compatibility with existing diesel infrastructure make it a cleaner and more sustainable option. Between 2021 and 2024, renewable diesel accounted for the largest share of credits at 31%, followed by ethanol at 26% and biodiesel at 23%. Since the introduction of renewable diesel in 2017, its share of credits has grown, while ethanol and biodiesel have declined from their 2016 levels of 62% and 33%, respectively.

To meet Oregon’s goal of a 20% reduction in CI by 2030, ICF developed two compliance scenarios. Scenario C, which incorporates multiple fuels for a more holistic approach, highlights the continued importance of renewable diesel and other low-carbon liquid fuels alongside the increasing adoption of zero-emission vehicles. Regulatory focus on zero-emission models positions them as the largest contributors to the carbon credit system, but renewable diesel and similar fuels will remain critical in meeting long-term targets.

Looking ahead, the CI of renewable diesel is expected to decrease further by 2030, driven by technological advancements, improved feedstocks, and supportive regulatory policies that promote low-carbon alternatives.

Sources

- Ckinetics article: Exploring the Disparity in

Renewable Diesel Adoption: Why Oregon Lags Behind California?

- BCG Report: What It Will Take to Reap the Rewards of Renewable Fuels

- Oregon Department of Environmental Quality Proposed Targets

- Oregon Clean Fuels program: https://www.oregon.gov/deq/ghgp/cfp/pages/quarterly-data-summaries.aspxNews Articles

- U.S. Department of Agriculture: Biodiesel and Renewable Diesel: What’s the Difference?

- Biofuels explained: Biofuels and the environment (US energy information administration)- (https://www.eia.gov/energyexplained/biofuels/biofuels-and-the-environment.php#:~:text=Lipid%20feedstocks%E2%80%94waste/used%20cooking,thus%20increase%20their%20carbon%20intensity.)

0 Comments